The production cost of cleaner fuel in aviation

Originally posted June, 2024

It’s a volume game.

Planes and ships are designed to transport large volumes over long distances. Not a cheap business to run. That means, you want to prioritise as much cargo as possible and minimise the space needed for fuel. To do that requires high energy density (even better if it doesn’t need to be compressed). Biofuels therefore need to be cheap, energy dense, cost stable, and derived from sustainable sources. Batteries can’t do long-haul routes (yet), so we have two options, hydrogen and biofuels.

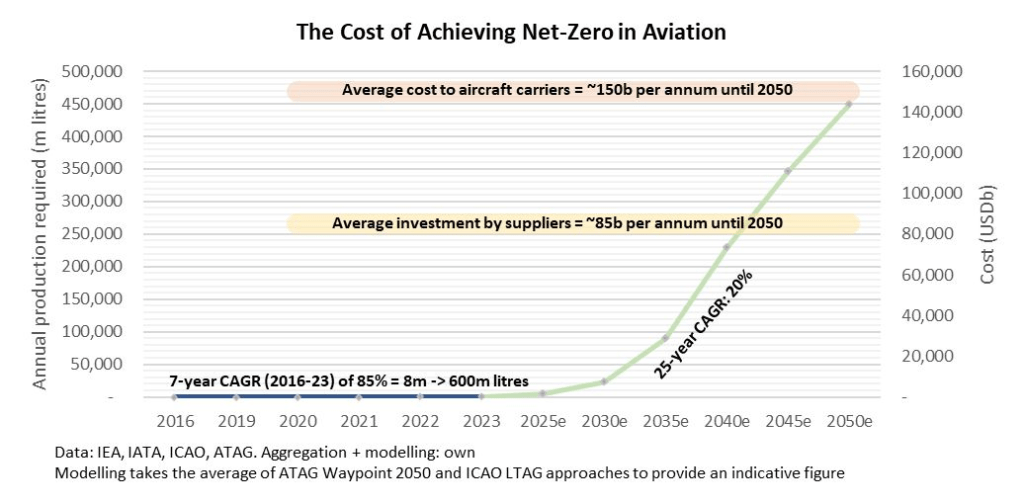

Production: The aviation industry consumes ~400 billion litres of fuel each year. Biojet fuel production has increased from 8 million litres in 2016 to ~600 million litres in 2023. Forecasting production is challenging but the International Air Transport Association (“IATA”), a major aviation trade association, forecasts production to reach 5 billion litres by 2025, the IEA does the same but by 2028 (or 15 billion litres in an accelerated scenario). Supply since 2016 has increased at a CAGR of 85% from a near non-existent base, and will need to grow at a rate of 25% for the next 25 years. The below chart, shows the exponential growth required until 2050 to decarbonise aviation.

Cost: The complete replacement of conventional jet fuel would require 170 new refineries and investment of US$60b+ each year. Production facilities have a time lag from planning to production of 3-5 years, there are currently 140 facilities that have been announced to be in production by 2030 – although many of these have not reached FID. The next 2-3 years will be pivotal in ensuring the necessary infrastructure is in place to meet short-term decarbonisation goals.

Acceleration: How can we reduce the cost of biojet fuels.

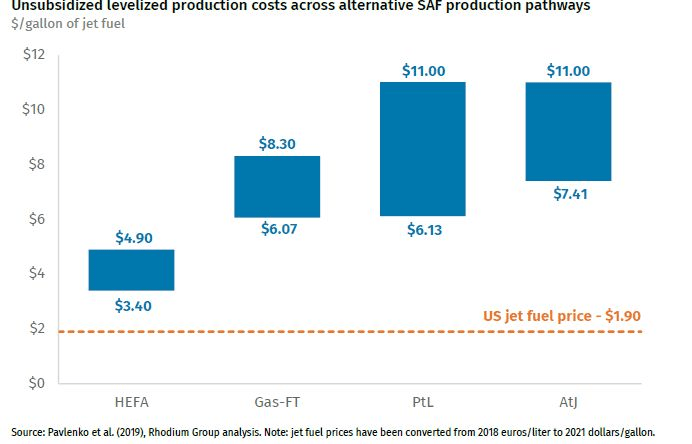

1. Feedstock costs and quality – 65% + of OPEX costs are due to feedstock procurement. However, ensuring feedstocks have lower levels of contaminants will reduce pretreatment and processing requirements.

2. Integration with brownfield sites – integrating infrastructure with brownfield upstream/downstream sites will create savings opportunities. For example, a biomass production facility may locate itself near a pulp or pellet facility to improve accessibility and efficiency. The same goes for a biorefinery locating itself near to a petrochemical facility to for distillation.

3. Product diversification – whilst biojet fuels will likely be the primary product, other products with a higher margin may also be catered to, thereby supporting overall production costs.

4. Policy – the carbon intensity and sustainability of a fuel is now having an impact on accessibility to fiscal incentives. Therefore, accessing these incentives is critical, focussing on the price of fuel relative to the emissions reductions offered can also yield greater benefits.

Leave a comment